Timing the market is an exceptionally challenging (if not entirely impossible) feat. Average investors consistently trail behind market indices, and even seasoned professional fund managers often find themselves falling short of their respective benchmarks. Both ordinary investors and professional fund managers have a difficult time pinpointing exactly when to make decisions about buying or selling securities. It proves to be a complex and nearly futile endeavor to accomplish consistently over an extended period of time. In this article, we’ll explain why and what you can try instead.

Market Timing Is Consistently Inconsistent

Timing the market usually involves attempting to “buy low and sell high” by analyzing current market trends for inefficiencies or volatility indicators. This strategy may work sometimes, but it is far from perfect. Not only do you have to guess when to buy in, but you then have to guess when to sell. That means for every gain, you have to be right twice to make timing the market worth it. Unfortunately, market bottoms can only be truly spotted in hindsight, and timing the market is risky and often closer to playing the lottery than it is to an educated guess.

Timing the Market Is Expensive

Timing the market can also be expensive. Depending on your account type, asset class, and where you are executing your trades, you will likely be charged for every purchase and sale you make, and that’s on top of any taxes owed on gains. The more frequently you trade, the higher your transaction costs will be.

In a taxable account, if you held the assets for a year or less, your gain will be taxed as ordinary income at your marginal tax rate, which can be as high as 37% for high-income earners. Long-term gains (for assets held for greater than a year) are taxed at a preferential rate. Regardless of your tax rate, your market timing must still be right more often than not just to cover the cost of your guess.

You Will Miss Out on Compound Growth & Market Rebounds

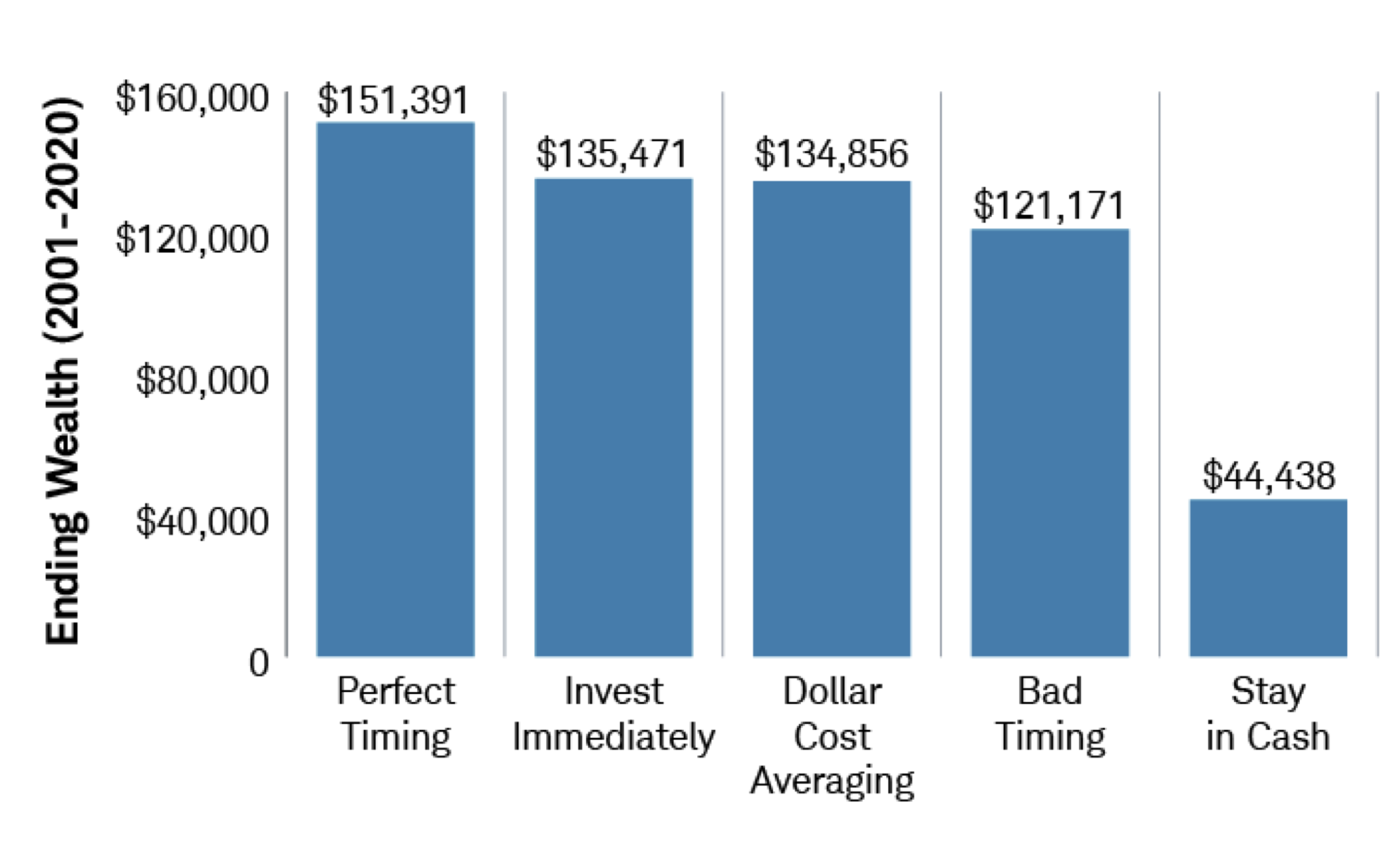

A recent study by Schwab Center for Financial Research found that bad market timing is worse than investing immediately, regardless of the market conditions at the time of investing. This indicates that even in market downturns, or just before a downturn, investors who invest immediately and remain invested will be better off than those who stay on the sidelines or attempt to time the market.

Take a look at Schwab’s graph below, which shows just how much more a fully invested portfolio earns over the course of 19 years. It would earn approximately $14,000 more in growth than a portfolio with bad market timing, and $91,000 more than a portfolio that stays in cash. The only investor who performs better is the one with perfect timing—but since we already know that perfect timing is virtually impossible, investing immediately is the next best strategy.

What’s more, over time that extra $14,000 or $91,000 will have the opportunity to grow even more thanks to compounded interest. Even if the market fluctuates in the short term, the odds are high that a solid investment strategy will grow over time.

Even bad timing trumps inertia

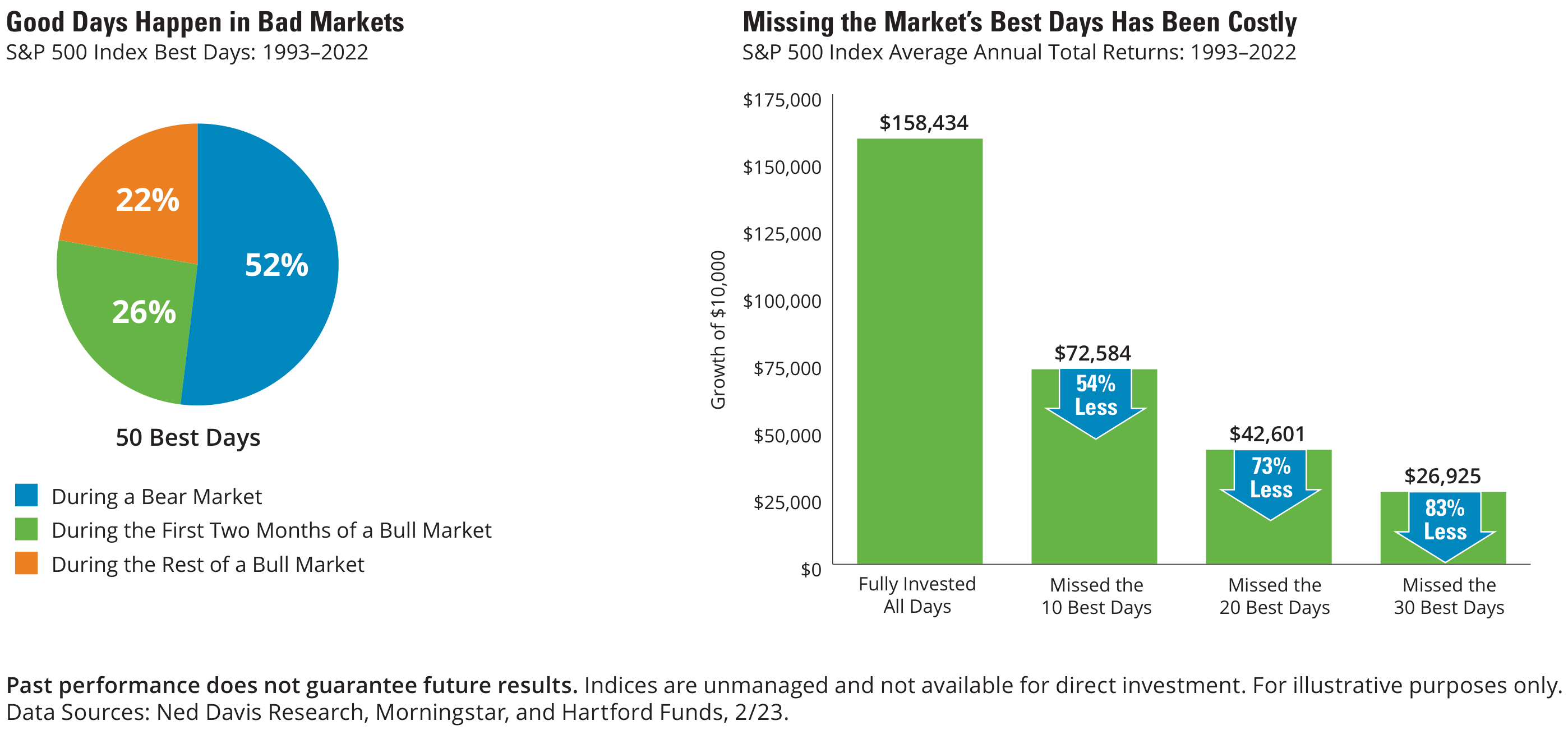

Another graph by Hartford Funds and Morningstar shows what happens if you miss the best days in the market, which often closely follow a major downturn and can be just as difficult to predict. An investor who missed the 10 best days in the market between 1992 and 2021 would have earned 54% less than someone who was fully invested during the same time period.

Someone who missed the 30 best market days would have earned a whopping $172,000 (83%) less than their fully invested counterpart. The research is based on a $10,000 initial investment, but these numbers would be much more dramatic if you were dealing with a $100,000 or even a $1,000,000 portfolio.

The time value of money tells us that a dollar today is worth more than a dollar tomorrow, and this is certainly the case when it comes to investing. The longer you are invested, the more likely you are to ride out the day-to-day market fluctuations and experience growth instead.

Today Is the Day to Start

Don’t deprive yourself of growth opportunities by trying to time the market prematurely. At Infiniti Wealth Management, we are dedicated to assisting our clients in optimizing their portfolios and helping them become comfortable with their long-term financial choices.

If you’d like to explore how we can guide you through market volatility and address concerns about market timing, please don’t hesitate to call our office at 845-278-8638 or send us a message to set up a complimentary consultation.

About Mike

Michael Durante is a founder, Certified Financial Planner™ (CFP®), and Certified Divorce Financial Analyst™ (CDFA®) at Infiniti Wealth Management, an independent, fee-only financial advisory firm. With over 25 years of experience, Mike specializes in serving women who are going through a life transition, whether that’s a divorce or the death of a spouse, as well as pre-retiree and retiree couples. He is passionate about helping his clients develop a personalized financial plan based on their values and goals so they enter retirement with confidence and peace of mind. Mike has both a bachelor’s degree in business administration and an MBA from Pace University. When he’s not working, Mike loves spending time outdoors hiking, biking, walking, golfing, campfires, the beach and doing yard work, as well as spending time with family and friends. Mike also enjoys to read, travel, and check out local restaurants and events. To learn more about Mike, connect with him on LinkedIn.

Posted:

September 13, 2023 - Michael Durante, CFP®, CDFA®